Why Your Budget Fails Every Month (And How to Fix It)

Your budget fails every month because you set unrealistic spending limits, forget irregular expenses, or stop tracking actual spending after the first week. The fix requires diagnosing your specific failure reason, adjusting category limits to match reality, and building a weekly review habit that takes 10 minutes.

According to a 2025 Bankrate survey, 54% of Americans still live paycheck to paycheck. A 2025 Debt.com Budgeting Survey found that nearly 7 in 10 consumers do not review their budgets regularly. Budgeting apps cost $10–18 per month, yet most people abandon them within two months. The problem is not the tool. The problem is the behavior. You need a system that matches your actual spending and a habit you can sustain long-term.

This article identifies the five main reasons budgets fail, provides a diagnostic checklist to pinpoint your specific problem, and gives step-by-step fixes for each failure reason. You will learn how to adjust unrealistic category limits without guilt, how to add sinking funds for irregular expenses, and how to build a weekly review habit that prevents budget drift. The article also explains when budget failure is actually an income problem that spending cuts cannot solve, and how long it typically takes to fix a broken budget.

The 5 Main Reasons Your Budget Fails Every Month

Most budget failures come from one of five root causes. These reasons overlap, but each has a distinct fix. Understanding which reason applies to you matters more than trying every fix at once. You save time by targeting the specific problem instead of rebuilding your entire budget from scratch. The most common reason is unrealistic spending limits, followed by forgetting irregular expenses.

Reason 1: Unrealistic Category Limits

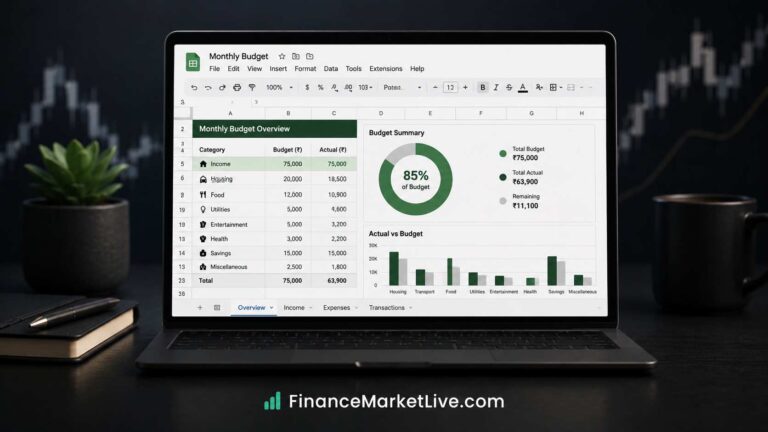

You budget $200 for groceries but spend $400 every month. This happens when you set category limits based on what you wish you spent instead of what you actually spend. The budget feels punishing from day one, so you abandon it. Unrealistic limits are the most common reason budgets fail within the first month.

The fix is to adjust category limits to match your actual past spending. Track your spending for one month without changing anything, then set next month’s budget based on what you learned. If you spent $400 on groceries, budget $400. You can work on reducing spending later, but start with reality. For specific strategies on reducing expenses without major lifestyle changes, see our article on how to cut monthly expenses by 20% without changing your lifestyle.

Reason 2: Forgetting Irregular Expenses (Sinking Funds)

Your regular monthly expenses fit within your budget, but unexpected bills like car maintenance, holiday gifts, or annual insurance premiums break your budget when they arrive. These are not emergencies. They are predictable expenses with irregular timing. When you do not budget for them in advance, you must pull money from other categories or use credit cards.

The fix is to add sinking funds for each irregular expense. Calculate the annual cost, divide by 12, and add the monthly amount to your budget. For example, if car maintenance costs $1,200 per year, budget $100 per month for car maintenance. When the bill arrives, you already have the money. For a detailed explanation of sinking funds with real examples, see our article on sinking funds and how they eliminate financial surprises.

Diagnostic Checklist: Which Failure Reason Applies to You

The following checklist helps you identify which specific failure reason applies to your situation. Read each symptom and mark whether it describes your experience. The diagnosis with the most checkmarks is your primary problem. Focus on fixing that problem first before addressing other issues. Trying to fix everything at once often leads to overwhelm and abandonment.

| Symptom | If Yes, Your Problem Is |

|---|---|

| I consistently overspend in one or two categories each month | Unrealistic category limits |

| My budget works until an unexpected bill arrives | Forgetting irregular expenses |

| I stop tracking spending after the first week of the month | Not tracking actual spending |

| I set up my budget once and never update it | Setting it and forgetting it |

| I use a budgeting method that does not match my income type | Using the wrong budgeting method |

| My income is not enough to cover my essential expenses | Income problem, not spending problem |

| I feel guilty about spending and abandon the budget | Unrealistic expectations about wants |

If you checked “Not tracking actual spending,” your main problem is the tracking habit, not the budget structure. Building a consistent tracking habit matters more than perfecting category limits. If you checked “Income problem,” cutting expenses will not solve the root issue. You need to increase income or reduce essential costs like housing or transportation. The next section covers this distinction in detail.

How to Fix Each Budget Failure Reason (Step-by-Step)

Each failure reason has a specific fix that addresses the root cause. The table below shows the fix action, how long it takes, and when you will see results. Start with the fix for your primary problem, then add other fixes as you build momentum. You do not need to implement all fixes at once. Consistent progress beats perfect execution.

| Failure Reason | Fix Action | Time Required | When It Works |

|---|---|---|---|

| Unrealistic category limits | Adjust limits to match actual past spending | 30 minutes | Next month |

| Forgetting irregular expenses | Add sinking funds for each irregular expense | 45 minutes | In 2–3 months |

| Not tracking actual spending | Build 10-minute weekly review habit | 10 minutes per week | In 3 weeks |

| Setting it and forgetting it | Review and adjust budget on the 15th of each month | 15 minutes per month | Next month |

| Wrong budgeting method | Switch to method that matches your income type | 1–2 hours | Next month |

Fix for Unrealistic Limits: Adjust to Match Reality

Open your budget spreadsheet or app and review your spending for the past two months. Calculate the average for each category. Replace your current budget limits with these averages. If you spent $400 on groceries, budget $400. If you spent $150 on dining out, budget $150. This adjustment removes the frustration of constant overspending.

After adjusting limits, pick one category to reduce over the next three months. For example, try to reduce dining out from $150 to $130. Make small, sustainable changes instead of dramatic cuts. Dramatic cuts create deprivation, which leads to budget abandonment. Small cuts feel manageable and build confidence. For a detailed method, see our article on zero-based budgeting and how to assign every dollar a job.

Fix for Forgetting Expenses: Add Sinking Funds

List every irregular expense you pay during the year: car maintenance, holiday gifts, insurance premiums, vacation trips, charitable donations, vehicle registration. For each expense, write the annual cost and divide by 12. Add the monthly amount to your budget as a sinking fund category. These categories are not optional. They are essential expenses with irregular timing.

If your total sinking fund contributions exceed your budget, prioritize by urgency. Car maintenance and insurance are high priority. Vacation and holiday gifts are lower priority. Start with high-priority sinking funds and add lower-priority ones as your budget allows. The goal is to spread annual expenses across 12 months so they do not break your monthly budget.

Fix for Not Tracking: Build a 10-Minute Weekly Review

Set a recurring calendar reminder for every Sunday at 7 PM called “Update Budget.” Open your budget spreadsheet or app and enter all spending from the past week. Check the difference column to see which categories are close to the limit. This takes 10 minutes. The weekly cadence prevents the backlog that happens when you try to track monthly.

Use the Google Sheets mobile app for quick updates throughout the week if you prefer. Open the app, tap the actual amount cell, enter the new total, and the difference updates automatically. This approach works better for people who forget to update their budget until the end of the month. For a step-by-step guide on building this spreadsheet, see our article on how to build a monthly budget in Google Sheets.

When Budget Failure Is Actually an Income Problem, Not a Spending Problem

Your budget fails every month if your essential expenses exceed your after-tax income. Essential expenses include rent or mortgage, utilities, groceries, transportation, minimum debt payments, and insurance. If these categories total more than your monthly income, no amount of spending discipline will fix the problem. You have an income problem, not a spending problem.

The fix for an income problem requires increasing income or reducing essential costs. Increasing income means getting a raise, finding a higher-paying job, or adding a side income stream. Reducing essential costs means moving to cheaper housing, refinancing a mortgage, or selling a car and buying a cheaper one.

These are major decisions, but they are necessary when expenses exceed income. A 2025 Yale Program on Financial Behavior study found that 38% of paycheck-to-paycheck households have essential expenses that exceed income, which means cutting wants will not solve their financial stress.

If your essential expenses are less than income but you still live paycheck to paycheck, the problem is sinking funds or wants spending. Add sinking funds for irregular expenses and reduce wants spending until you build an emergency fund.

Once you have an emergency fund, focus on increasing income to accelerate savings. The Consumer Financial Protection Bureau recommends prioritizing emergency savings before aggressive investing, which protects you from going into debt when an unexpected expense arrives.

Timeline for Success: How Long Until Your Budget Works

Most people succeed with budgeting after three months of consistent tracking. The first month feels difficult because you are learning your spending patterns and adjusting category limits. The second month feels easier because you know what to expect. The third month feels manageable because the weekly review habit is established. By month four, budgeting becomes automatic instead of effortful.

Research from behavioral finance shows that habit formation takes an average of 66 days, which is about two months. This means you should expect to feel deliberate effort for the first two months before budgeting becomes automatic.

If you abandon your budget before day 60, you will never reach the automatic phase. Give yourself three months before judging whether budgeting works for you. Track consistency, not perfection. Missing one week or overspending one category does not mean failure. Getting back on track the next week is what matters.